Rural Communities and Land Reform

The adoption of the law on turnover of agricultural land is a historic step for Ukraine.

Although today it is more of psychological significance and one still has to wait quite a long time for real economic benefits, since the market will be as restricted as possible until 2024, it is crucial to have no less important bills on land reform adopted by the Verkhovna Rada within the following two weeks.

In particular, the decentralization of land relations (transfer of state-owned agricultural land into communal ownership and transfer of land governance powers to the local level) will improve the quality of land governance. It will significantly increase tax revenues into local budgets, which is necessary for the development of rural communities on condition of their growing autonomy in the framework of decentralization reform.

Rural communities, land, and agrarian sector

Land is one of the main resources of rural development. Village communities receive budget revenues from various taxes generated by farmland in different ways and from leasing state / communal agricultural land. Owners of land parcels or shares have income from leasing their land to farmers. Also, a considerable part of income of rural residents comes from self-employment on land (sale of agricultural products), employment in agri-companies and non-monetary profits in the form of the value of consumed products from their own gardens. Yet, opportunities for non-agricultural employment and income in rural areas are very limited at present.

The following interesting observations can be clearly made from the available statistical data:

- Villages are considerably poorer than cities. Rural residents are serously behind urban population by income level. Figure 1 shows that poverty in villages is considerably higher than in cities, and the gap is growing: in 2018 it was 11 relative points (four times growth in the last 20 years).

- Agriculture is a kind of spineback of rural economy, yet it is insufficiently contributing to the well-being growth of rural residents. Figure 2 shows that agriculture has been growig much faster than the real income of rural residents.

- Village development has been seriously suffering from under-funding of the budgets of village communities. It has many reasons, but inefficient land management, no land market, and undervaluated land are among the main ones. These will be explained in more detail below.

Figure 1. Poverty level by relative indicator, %*

Source: Our own presentation based on the data from the Institute of Demography and Social Research, the National Academy of Sciences of Ukraine

Figure 2. Dynamics of real income of rural population and added value in agriculture

Source: Our own presentation based on data from the State Statistics Service of Ukraine

Budgets of village communities and land

Moratorium on agricultural land turnover and normative monetary valuation of land lower “land” income of communities.

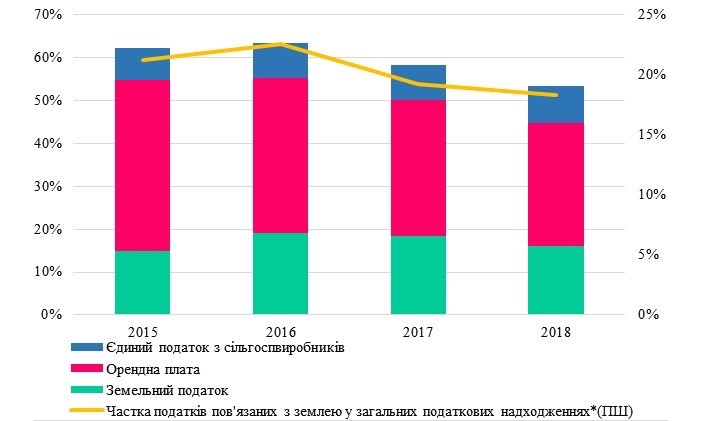

The budgets of village communities are currently over-dependent on transfers from the State budget – 60-80% on average (the rest is generated by their own taxation and non-taxation revenues). Land generates the following revenues to local budgets:

- land tax

- rental payment for state and communal land

- fourth group single tax for agri-producers, and

- individual income tax received from land lease.

Around 11% of total revenues in local budget are made of revenues from local taxes and fees (Figure 4). More than 50% are generated from land-related sources. The latter include rental payment for state and communal land as the most considerable one (Figure 5).

A serious problem of “land” taxation is its base, that is, normative monetary valuation of land (for all the above-mentioned sources of income items, except for Individual Income Tax on land lease income**). It is the level of normative monetary valuation that is one causes of the significant underperformance of land-related revenues by rural communities due to the imbalance between the actual normative monetary valuation (NMV) of land and actual added value in agriculture.

In Ukraine, (Figure 3) the rate of NMV increase (regulated in an administrative way) is considerably behind the profitablity growth of the agrarian sector. Because the NMV “cannot keep up” with the profitability growth, farmers have been giving smaller and smaller portions of their income as taxes and fees. Moreover, in 2018 the NMV has even decreased on average (according to the new Methodology), which lowered the nominal tax burden on farmers.

Figure 3. Dynamics of actual added value In agriculture and normative monetary valuation (NMV)

Source: World Bank WDI (2018), StateGeoCadastre, and State Statistics Service

Paradoxically, the moratorium on the purchase and sale of agricultural land is the fundamental reason for the situation with normative monetary valuation, as the lack of a market causes the absence of a market price, and hence the need for such an artificial structure as a normative monetary valuation for taxation purposes. The opening of land market should help resolve the problem of deflated tax base, since it will be possible to rely on the market value of land when calculating tax liabilities and bring the latter closer to a fair (higher) level. Of course, given the extremely limited land market, before 2024 it is difficult to hope for a fair price due to a rather limited demand. However, starting from 2024 we can expect a significantly higher demand and, consequently, coming closer to a fair value of land. Model calculations prove that if a liberal land market with a minimum of restrictions and support for farmers was implemented from the very beginning, one could expect a twofold increase in the value of land.

Figure 4. Structure of local budget revenues

Source: The author’s presentation based on annual reports from the State Treasury Service of Ukraine

Figure 5. Share of land-related tax revenues within internal (one’s own) and total tax revenues of local budgets

Source: The author’s presentation based on annual reports from the State Treasury Service of Ukraine

Low level of land governance in Ukraine accounts for low budget revenues

Another important reason why local budgets do not receive revenues generated by land is inefficient land governance, which is evidenced with a significant share of unregistered land. In total, according to the StateGeoCadastre, the average share of unregistered lands is about 28% of the territory across Ukraine (Figure 6).

Figure 6. Share of unregistered land, %

Source: The author’s presentation based on the StateGeoCadastre data

The patches on the map are village and township councils, according to the administrative structure of Ukraine. The figures in square brackets are the percentages of unregistered land. The numbers in parentheses are the number of village and township councils.

In order to empirically verify the relationship between the share of unregistered land and tax revenues from the above-mentioned four revenue items, we built a nonparametric model and graphically reflected the relationship between the percentage of unregistered land and tax revenues per hectare and the level of budget execution under these items (Figure 7). As we can see, a rather strong negative correlation exists between the amount of tax revenues generated by land and the share of unregistered land.

Figure 7. Correlation of land-generated budget revenues (per ha – vertical axis) and share of unregistered land (horizontal axis)

How land reform strengthens the development capacity of communities

As has been repeatedly stated, land reform is not limited to Bill No.2178-10 on agricultural land turnover, but it includes a package of at least 8 bills under the parliament’s consideration at present and a set of measures to increase the transparency of land governance. In particular, mandatory registration of land transaction prices, development of the Land Governance Monitoring System and the Agrarian Registry, establishing of a Credit Guarantee Fund, etc. The proposed package of bills will resolve the above-mentioned problems as follows.

1) Moratorium and normative monetary valuation

Bill No.2178-10 abolishes the moratorium and, together with other laws, launches a civilized turnover of agricultural land. The expected main effects include increased rental prices and agricultural land cost and the emergence of a “normal” market price. Once a market price is in place, it will be possible to start using it as a tax base and thus generate fair tax revenues from each hectare of agricultural land. Of course, the bill approved on March 30 postpones all this until 2024 at least, but such a progress of events is inevitable.

2) Higher quality of land governance

In this area, “working front” of the land package is quite broad and, first of all, it aims at increasing the efficiency of using state and communal lands, which are currently a source of mass corruption and large budget losses. The solution to this problem can be designed like this:

- Transfer of approximately 5.5 million hectares of state-owned agricultural land (out of the available 7.2 million ha) located outside settlements into communal ownership of communities as part of the decentralization reform. Also, the transfer of land management functions from the StateGeoCadastre to the local level (Bill 2194). This will give rural communities additional development resources and an opportunity to better manage land resources locally.

- Setting rules for land distribution when privatizing agricultural land of state and communal companies (Bill 3012-1, up to 3 mln ha). When privatizing this type of agricultural land, it is proposed that:

- up to 40% of the total area of the agricultural land be transferred into private ownership of the company employees free of charge;

- up to 20% of the total area of the agricultural land be transferred into the ownership of the participants of the Anti-Terrorist Operation and the United Forces Operation free of charge;

- no less than 40% of the total area of the agricultural land be sold or leased via transparent land auctions.

- State and communal land will be sold or leased exclusively via transparent land auctions (Bill 2195).

Taking into account the adopted draft law No.2178-10, it is highly probably to talk only about leasing state and communal agricultural land, as the sale of state and communal agricultural lands is indefinitely prohibited. Yet, the effectiveness of land auctions is quite impressive. Since 2016, the sale of lease rights to state-owned agricultural land has been done exclusively through land auctions. This has led to a significant increase in the rental cost of state-owned land. In 2016, the price of auction-based land lease was UAH 2,249.80/ha, whereas the price for renting state land on a non-competitive basis, according to earlier agreements, was only UAH 940/ha. For comparison, an average rental price for private agricultural land (the so-called “land shares”) in 2016 was UAH 1093.40/ha against UAH 862/ha in 2015. Moreover, the gap between the rental prices for private and state land widened in 2018 (UAH 3,431.50/ha is the average price for renting state-owned agricultural land via auctions).

Thus, the launch of a fully-operational land market through the proposed package of land laws and other accompanying measures should become a significant stimulus to the development of rural communities. Decentralization of land relations (transfer of state agricultural land into communal ownership and transfer of land management powers to the local level) will improve the quality of land governance. It will be a strong driver for growing tax revenues into local budgets. This is especially needed for the development of rural communities in the context of their increasing independence within the decentralization reform.

The pilot launch of the Agrarian Registry is an important step towards overcoming the problem of unregistered land, which is one of the factors accounting for the gap between the actual and the economically possible levels of budget revenues. Lifting the moratorium and opening free market turnover of agricultural land will create the necessary conditions for calculating tax liabilities based on the real (market) value of land. This is an important factor for the growth of local budget revenues.

* Relative poverty level is the share of people whose income level is below 75% of the median level of per capita equivalent expenditures for the population of Ukraine on the whole (i.e., lower than 75% of the expenditure level, which is in the middle of the growing level of the average expenditures per capita)

** The tax rates are the following: 1% is the maximum rate of land tax for agricultural land, but the actually applied rate is much lower than 1%; 0.95% is the maximum rate of the 4th group single tax, and single tax payers are exempt from land tax on rented or their own land, as well as from income tax. No less than 3%, but no more than 12%, is the rental rate for state and communal land. In most communities, the rates of local taxes and fees have not been set at the maximum level. In any case, tax rates remain relatively stable, and the dynamics of revenues to local budgets fully depends on the dynamics of normative monetary valuation.